What is asset tokenization on a blockchain?

Asset tokenization is an extended use case of blockchain technology beyond Bitcoin (BTC) that enables the purchase, sale and exchange of digital assets on the distributed ledger. For instance, real estate asset digitization contributed to developing an illiquid asset, allowing buyers to transact immutably. But what does tokenization mean in crypto?

The tokenization of assets is the process of issuing security tokens (a type of blockchain token) representing real digital tradable assets. Like an initial coin offering (ICO), security tokens are issued via a security token offering (STO) process, through which investors can buy payment, equity or utility tokens.

However, it is essential to note that tokenization differs from the securitization of assets. For example, the securitization process involves pooling specific illiquid asset classes so they can be repackaged into securities. So, what type of assets can be tokenized? Virtual or real assets can nearly all be converted into digital tokens through tokenization. For instance, security tokens issued via the STO process may represent an investment fund, company shares or real estate ownership.

This method can transfer off-chain real-world assets' economic worth and ownership rights into blockchain-based tokens. Furthermore, asset tokenization may help alternative financing models overcome infrastructure development barriers, given the rapid transfer of infrastructure to intelligent systems and the desire to unleash efficient finance.

However, blockchain technology and related asset tokenization are still in their infancy; therefore, challenges must be surmounted before they are widely adopted. This article explains asset tokenization on a blockchain, how it's done and why it might upend several industries, especially the real estate and financial sectors. In addition, the process of converting real assets into digital assets and the difficulties of putting asset tokenization into practice are also examined.

How does asset tokenization work?

If you want to know how to tokenize an asset, the first thing to understand is the role of smart contracts in turning real assets into digital assets. Digital tokens backed by underlying assets are controlled and executed using a smart contract. The conditions of the parties' agreement are put into lines of code already present on the blockchain network, making the smart contract a self-enforcing and self-executing contract.

Once the contract conditions are fulfilled, tokens can be delivered to investors directly through a smart contract, offering participants transparency, accuracy and efficiency by making contractual terms and historical data publicly available.

In technical terms, asset tokenization refers to developing an informatic code that highlights the essential elements of the asset while also providing some methods that enable the user to interact with the digital representation of the asset. This informatic code is created in Solidity for the Ethereum blockchain. In general, the asset tokenization process can be broken down into the steps below:

Choosing the asset representation model

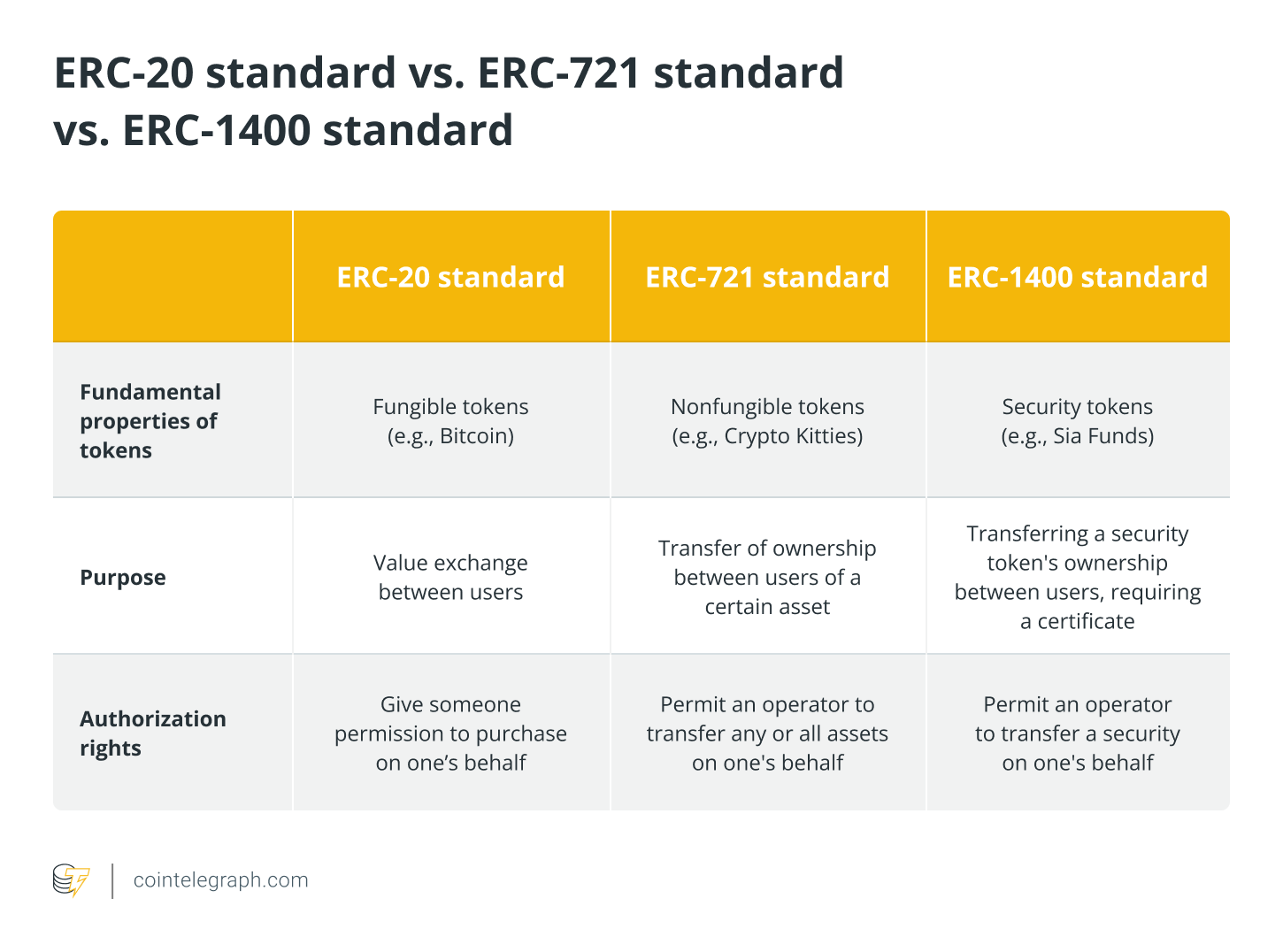

The Ethereum community has developed several token standards to represent various asset types. The adoption of distributed digital assets is made simpler by establishing these standards, allowing for interoperability between different blockchain projects.

An asset's unique characteristics can be represented by a collection of established functions called a token standard. The asset's fundamental properties, such as whether it is fungible or nonfungible, should be evaluated before deciding which token standard to use. The following table describes the most common token standards:

Additionally, maintaining privacy is a vital factor to consider when deciding how an asset should be tokenized. As transparency is introduced by default by blockchain, not all use cases and sectors can embrace this transparency. However, technologies like zero-knowledge proofs can help mitigate this issue, especially for private blockchains.

Modeling the asset

Various aspects should be taken into account before implementing the token model chosen for representing assets so that it is clear which data will be saved on-chain and off-chain. For example, any legal or regulatory restrictions on data privacy, the degree of data trust and scaling needs should be considered while developing the specific code and token behavior.

Proper engineering is necessary for tokenizing financial assets during issuance, liquidity management, etc. A term sheet document should contain details about the token's behavior as regulators may require issuers to issue digital assets.

Review of the informatics code's technical and security aspects

It is crucial to conduct a smart contract audit with standardized methods or by requiring expert third parties to assess and certify the informatic code before it goes online.

The deployment of the informatics code

After completing a security evaluation, the code can be deployed on the blockchain, either public or private, depending on the use case and perimeter under consideration. Users should be able to transfer and store these tokens after the deployment of the informatic code.

But how much does it cost to tokenize an asset? Asset tokenization platforms charge between $30,000 and $100,000 or maybe more, depending upon the chosen features of the tokens. On average, tokenizing the assets may take 3–6 months.

Post-tokenization management

The token owners receive future dividends and interest payments from tokenized assets in the form of cryptocurrency or equivalent fiat money in their wallets. Furthermore, digital token issuers are also responsible for the accounting and taxation of these tokens as well as making financial reports.

The benefits of asset tokenization

The token economy helps digital token issuers reduce the friction of creating, purchasing and selling securities. For instance, illiquid tangible assets such as fine art or intangible assets like real estate can be traded on the secondary market, offering greater liquidity to sellers and investors.

Additionally, an immutable record of ownership along with the rights of the concerned parties are embedded directly onto the token, allowing sellers and investors to find out details like the original owner of the token, current dealer(s), etc. Furthermore, the automated smart contracts help to decrease transaction fees as well as faster processing of transactions by reducing the administrative burden of reviewing and validating transactions.

Also, straightforward send-and-receive transaction settlement and clearance can be automated, enabling quick transactions of only a few seconds instead of the hours or days previously needed. As a result, managing tokenized assets improves market efficiency and optimizes the exchange of goods and services.

A larger spectrum of people can buy/invest in tokenized assets due to the reduced minimum investment amount. Blockchain technology also allows asset tokenization startups to access tokenized funds without the involvement of third parties. Moreover, as security tokens are liquid, investors can exchange them 24/7 on the global secondary markets.

Risks associated with asset tokenization

Despite the above advantages, asset management in the token economy is not without risks. For instance, investors may suffer significant losses in the event of illiquid/low liquidity assets as market prices may be highly variable and can materially deviate from the fair value of a company or an investment opportunity.

The volatility risk of virtual assets is further increased by regulatory changes, cyber-attacks and crypto heists.

In addition, payment, utility and security tokens suffer from a valuation risk. For instance, assigning payment tokens an objective value is challenging because payment token prices are determined by global supply and demand dynamics rather than the standard methods of valuing assets such as discounted cash flows (DCF). DCF refers to a method of valuation that calculates an investment's value based on its anticipated future cash flows to evaluate the present value of an investment.

Similarly, as utility tokens stand for the right to use a product or service in the future, there are no tested techniques for valuation. Also, since many companies requesting tokenized funds are private, non-public companies not listed on a stock market, security tokens bear liquidity risk. Moreover, digital assets go through periods of reduced liquidity or illiquidity; as a result, in some market circumstances, it can be difficult or impossible to liquidate a position.

Asset tokenization platforms mostly rely upon open-source software for development purposes, exposing tokenized assets to theft, programming errors and cyber attacks. In addition, a digital asset may become unstable due to a hard fork and restrict users from using it as a long-term medium of exchange.

As with private equity or debt investments, the credit and counterparty risk, such as bankruptcy of the underlying issuer, is significant in the case of tokenized securities. Additionally, the operational risk may arise if digital assets are sent to the wrong distributed ledger address, resulting in a complete and irreversible loss of funds. Therefore, before confirming a transaction, users must always verify that the destination blockchain address is accurate.

Prerequisites for tokenizing assetsAlong with the risks mentioned above, regulatory challenges arise with blockchain-based de facto decentralized platforms, which need to be addressed for the broader adoption of the token economy. For instance, security regulations concerned with security tokens vary from jurisdiction to jurisdiction, preventing the free and global exchange of tokenized assets. For the full potential of the token economy to be realized, clear regulations for security tokens are essential.

In addition, the role of financial institutions in the value chain of tokenized assets should be clarified beforehand. For instance, they may act as advisors by offering token design consultation or leveraging their expertise as custodians. Platform integration is another crucial factor that may lead to wasting organizational resources if the chosen platforms cannot collaborate with the underlying business model.

Moreover, Know Your Customer (KYC) guidelines and laws like the Anti-Money Laundering Directive 5 (AMLD5) are at the center of any institution offering financial services to customers. Therefore, digital token issuers must follow KYC and AMLD5 regulations to operate as compliant service providers.

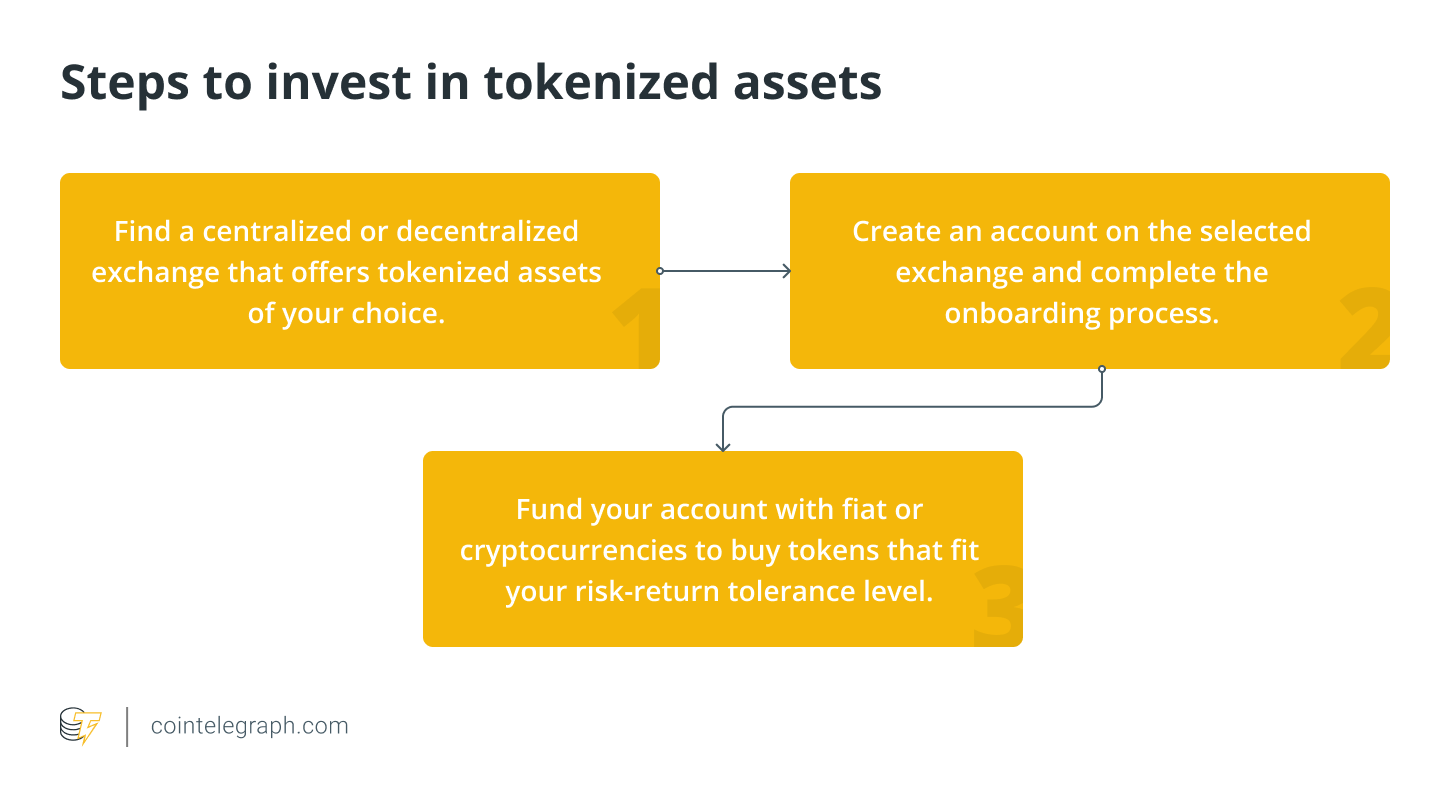

How to invest in tokenized assets

Investing in tokenized assets involves a process similar to that required for cryptocurrency trading. Some of the key steps are listed below:

Through an example of buying IHT Real Estate Protocol (IHT) on Coinbase, let's understand the steps of investing in tokenized assets more clearly:

Asset tokenization vs. securitization

The process of refinancing assets by a special purpose vehicle (SPV) in the capital market is called asset securitization. An SPV may qualify as a bankruptcy-remote entity since its activities are limited to acquiring and financing particular assets or initiatives. On the other hand, the process of creating a distinctive digital representation of an asset is known as asset tokenization.

The use of smart contracts, or programmability, distinguishes securitization from tokenization. Additionally, tokens may be traded in fractions, as there can be up to 18 decimals in an Ethereum token. Tokens can be kept directly in the buyer's wallet instead of the buyer indirectly holding assets.

The legal systems of the United States and Europe categorize tokenized assets as security tokens. That said, a financial instrument made out of a pool of token assets, such as leases, is known as a tokenized asset-backed security.

The activities of concerned parties can be more transparent through asset tokenization than securitization, which may lead to a higher valuation. Furthermore, the likelihood of asymmetric information would be lowered by the transparency of holdings in smart contracts. For instance, real estate can be tokenized and fractionalized in quick transactions with minimal regulatory overhead down to a square centimeter or even smaller.

Future of tokenized assets

Tokenization is a logical progression in the growth of securitization made possible by blockchain technology. Distributed ledgers enable unprecedented transparency, transactional efficiency, and risk control. In addition, it can make previously untradeable asset classes liquid, significantly increasing financial involvement and information efficiency in these markets.

In the future, we should anticipate seeing increasingly innovative and value-creating tokenization applications, especially in assets previously unavailable or only available to a select group of investors.

Movie rights or investments in natural resources, such as mining rights, may be among them. Virtually any asset may be domiciled, and its cash flows or future appreciation divided in a fully automated, transparent, regulated and essentially cost-free manner, thanks to the power of blockchain and tokenization.

Disclaimer : The above empty space does not represent the position of this platform. If the content of the article is not logical or has irregularities, please submit feedback and we will delete or correct it, thank you!

COPYRIGHT © 2021-2025 HZD.COM ALL RIGHTS RESERVED